By David Krupp, Global CEO, billups

Out-of-home (OOH) revenue is growing. Its share of total ad spend is not. This distinction matters more than the industry seems willing to admit.

Industry associations and analysts continue to report OOH revenue growth quarter after quarter, and we’re all quick to celebrate. Trade headlines highlight record investment. Industry bodies emphasize momentum. Media owners point to resilience in a world where most linear channels are shrinking. But this perspective obscures uncomfortable truths that no one is talking about and leaves media buyers’ most important questions unanswered.

Growth Without Share Increase is Not the Same as Progress

By any traditional measure, OOH looks healthy. In the U.S., OOH revenue surpassed $9 billion in 2024 (last full-year reported figures), marking one of the strongest years on record and extending a multi-year growth streak. During the same period, linear television, print, and radio continued to contract.

That puts OOH in rare company as one of the only legacy, linear media formats still growing in absolute dollars.

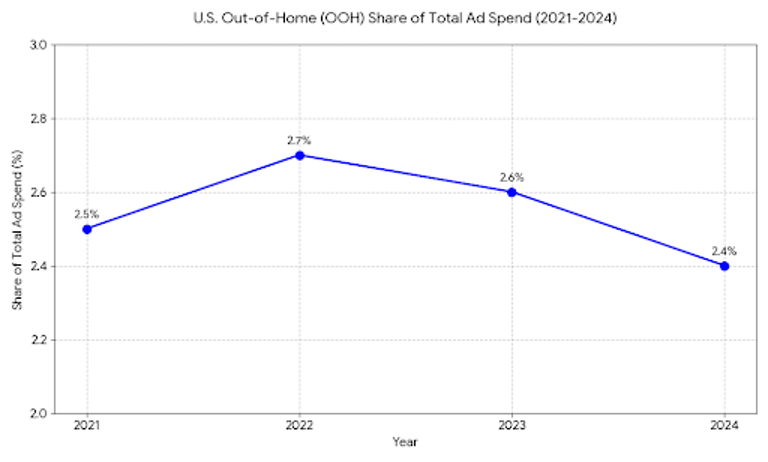

But revenue growth alone is not a reliable indicator of media vitality. When benchmarked against total advertising spend, roughly $380 billion in the U.S., OOH consistently represents between 2-3% of total ad spend, a figure that has remained remarkably unchanged for the past four years. In an advertising ecosystem defined by competition for marginal dollars, flat share is not neutral. It is a warning signal.

Figure 1:

Source: OAAA, Magna Global, and Insider Intelligence/eMarketer reports.

Source: OAAA, Magna Global, and Insider Intelligence/eMarketer reports.

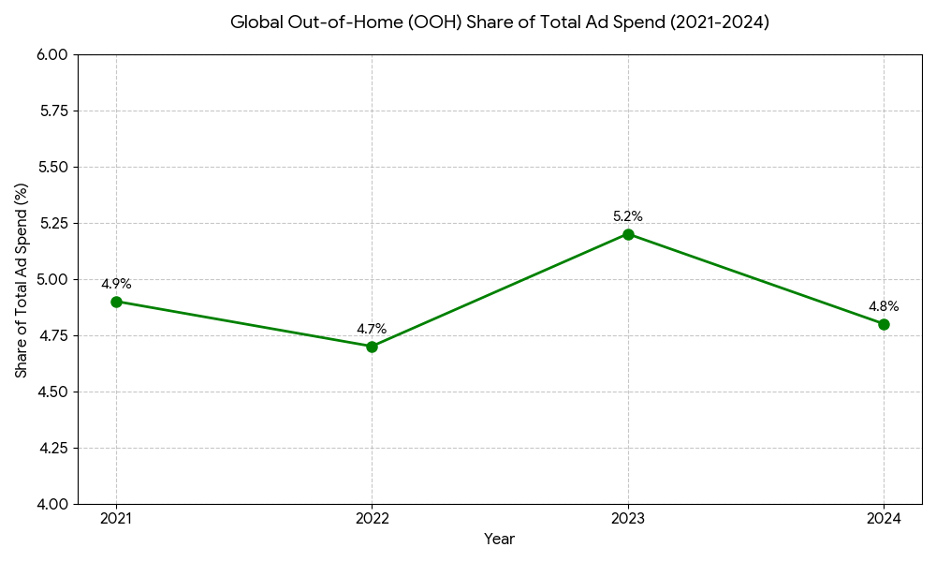

Figure 2:

Sources: 1. World Out of Home Organization (WOO) – Global Expenditure Reports (2024 & 2025) 2. Magna Global – Advertising Forecasts (Winter 2024 Update) 3. Zenith Media – Advertising Expenditure Forecasts

Sources: 1. World Out of Home Organization (WOO) – Global Expenditure Reports (2024 & 2025) 2. Magna Global – Advertising Forecasts (Winter 2024 Update) 3. Zenith Media – Advertising Expenditure Forecasts

The Buyer Problem the Industry Rarely Names

CFOs and brand leadership allocate incremental media investment to channels that demonstrate impact. They buy based on attributed outcomes, sales growth, and confidence that every additional dollar allocated will produce additional business results. This is where OOH’s celebratory narrative begins to break down.

While digital channels, particularly retail media, connected TV, and commerce-linked video, continue to advance their attribution frameworks, OOH’s industry-level messaging still leans heavily on growth, reach, and legacy value arguments. U.S. digital advertising revenue reached roughly $259 billion in 2024, growing at a mid-teens rate. Those dollars are moving because digital media is perceived, rightly or wrongly, as more accountable. OOH cannot afford to be the channel that everyone likes but few feel compelled to invest in more aggressively.

The industry’s optimism is amplified by trade bodies whose governance and funding structures are inherently supplier-aligned. Revenue growth is a clean, uncontroversial metric that benefits media owners and reassures insiders. But buyers’ most important concerns remain unaddressed. What they want to hear is why they should spend more in OOH, what incremental spend can do that other channels cannot, and how OOH can meaningfully change brand and performance outcomes.

Flat Share is the Real Strategic Risk

The danger is that OOH growth becomes capped, a reliable but secondary channel with a role defined by habit rather than demonstrable impact. In a world of expanding media options, flat share eventually becomes relative decline. If OOH cannot make a compelling case for incremental budget growth, it risks being overtaken by channels that provide any promise of directly connecting spend to outcomes. Retail media is the most obvious example, but not the only one. This is not a channel problem. It is a positioning and measurement problem.

The Conversation the Industry Should Be Having

The strategic question should not be “how do we keep growing revenue?” OOH is proven to drive foot traffic, app downloads, and sales transactions, yet the share of spend suggests OOH is only considered as an awareness media. The question amidst continued revenue growth should be “what is holding the media back from realizing its true and full potential?” The answer: Creating conviction that OOH is the format where competitive differentiation, creative potential, and measurable outcomes can scale.

Ironically, the structural case for OOH has never been stronger. Broadcast-level reach in an increasingly fragmented media environment, physical presence that cannot be skipped or scrolled past, increasing flexibility through digital formats, and resilience against signal loss and cookie deprecation. The problem is not the asset. It is the story being told about it and consistent validation of the outcomes it generates, alone and in concert with other media.

Stability is Not a Strategy

OOH needs better ambition. Celebrating revenue growth is understandable, but without a parallel data-driven push to explain why OOH is undervalued and a strategic opportunity for brands, we risk mistaking stability for long-term success. Revenue is a lagging indicator. Share is the strategic signal.

Until the industry starts talking seriously about share, what drives it, what limits it, and how to grow it, OOH’s future will be defined more by comfort than conviction. This would be a missed opportunity for one of the most durable, distinctive media channels available to marketers.