By Chris Buckley, SVP Business Development & Marketing, RAPP and Code

The economic impact of the pandemic has not been spread equally. Hard-hit industries like travel, retail and automotive were forced to rethink fundamental principles underpinning their normal business practices. While some faced hardships due to a prolonged disruption in trading, others capitalised on this new digital-first environment.

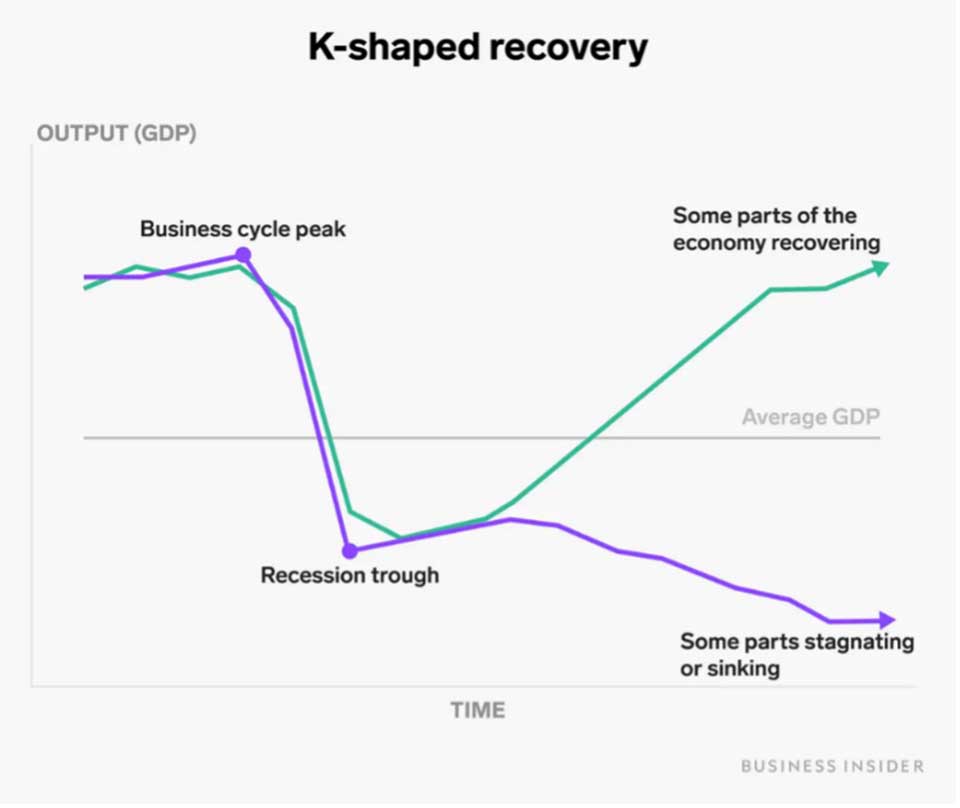

This phenomenon is known as a K-shaped recovery. Some brands and sectors are in a period of rapid growth, while others are headed for (or are already in) decline. This recovery model explains the success of digitally native brands and the failure of more traditional bricks-and-mortar businesses.

How different sectors performed in 2020

To better understand the impact of COVID-19 on consumer spending habits, here at RAPP and Code, we commissioned a nationally representative research survey for the UK market. Polling 1,000 consumers, we investigated six key sectors: Automotive, Consumer Technology, Financial Services, Luxury, Retail, and Travel, to uncover what Brits really think about the influence of COVID-19 on their current and future shopping habits.

Believe it or not, one-third of consumers say they plan to shop less in these six categories in 2021. This seismic realignment in spending means that brands will have to work smarter if they wish to capture new audiences, retain existing customers and drive continued loyalty.

Drilling down into the figures per sector, the findings show that travel and luxury will be hit hardest, with 41% and 34% of consumers saying they will spend less in these spaces, respectively. However, the cuts don’t stop there as respondents also report intensions to reduce spending in retail (31%), automotive and technology (both 30%) as well as financial services (27%).

The K-shaped recovery poses a troubling, divergent economic future, one where the economy rebounds unevenly, where certain industries and companies pull out of a recession while others stagnate or sink.

Thankfully, we believe there is an answer.

Enter individualisation

Brands talk a lot about personalisation, but it’s time marketers moved beyond that concept towards a new goal of individualisation. It’s a communications strategy that can be the cornerstone of deeper relationships with the consumer, based on a far richer understanding of an individual’s contextual needs, inferred motivation, and personal traits.

When questioned on the value of individualisation, 57% of consumers said they would spend more money with a brand that treats them as an individual. Younger generations are even more bullish, with 89% of 16-24-year-olds and 77% of 25-34-year-olds saying they would spend more money with a brand that treats them as an individual.

But nearly half (49%) of consumers said that all six sectors did a bad job at delivering individualised marketing communications in 2020.

Collectively, these insights point to a compelling truth: at a time when consumers plan to reduce spending in 2021, we now have clear evidence to show that individualisation can not only encourage consumers to spend more with your brand – but that this increase could lead to an average expenditure of 58% or more.

To provide the most relevant and contextual insights, we asked consumers to score each individual sector on how good a job they did at delivering individualised marketing communications.

Retail emerged as the clear winner, with 33% saying the sector delivered on their individual wants and needs. Luxury performed the worst, with only 10% believing the sector did a good job at communicating to them as individuals. Automotive and travel similarly ranked low, with 11% and 12% respectively, while financial services and technology scored 18% and 19%.

So, what can brands do?

Preparing for the new world

Individualisation, as is clear from our findings, has a key role to play in how brands reach, engage and connect with consumers. The brands that can structure, analyse and harness data to address individual consumer wants and needs will likely be the ones that come out on top.

No wonder retail scored better than the rest on individualised communications. Many brands in that space have advanced data capture and CRM functionalities, so it makes sense they’ve done an exceptional job at delivering on people’s wants, needs and behaviours.

At a time when consumer needs are changing, having the ability to predict customer behaviour and target people based on a unique set of attitudes, behaviours and beliefs will be key.

This is the ultimate goal for brands that have adopted a more digital-centric mindset in the wake of the pandemic. Being able to make sense of data and pull out the insights that matter most will prove a difference-maker when it comes to customer acquisition, retention and loyalty.

In short, individualisation has never been more important. By making smart, data-driven decisions, brands can employ the best aspects of automation and marketing science to reduce costs while maintaining margins.

Conclusion

At a time when every business decision is critical to the success or failure of an organisation, being able to leverage the power of individualisation is a key difference-maker that can help brands navigate uncharted waters and deliver results over and above the competition.